Contents

Last updated: Nov. 18, 2021

UPDATE: The TFSA limit for 2022 has been announced – please go to our new blog post: “What’s the TFSA limit for 2022?”

Now that you’ve entered a new year and finally put 2020 behind you (what a relief!), it’s a good time to plan for your tax-free savings account (TFSA) contribution.

The Canada Revenue Agency (CRA) announced a new TFSA limit for 2021. We review the TFSA rules below and how to take advantage of this savings and investing option.

What is a TFSA?

A TFSA is a registered investment or savings account that lets your money accumulate tax-free.

If you use the TFSA to invest your money, any investment income in the account, and capital gains, are also tax-free.

This handy account will shield your money from taxes as it grows. And you won’t be taxed on withdrawals, so it’s a flexible option if you think you’ll need to withdraw funds sooner rather than later.

What is the TFSA limit in 2021?

The TFSA program began in 2009. Any Canadian who is 18 or older, and has a valid social insurance number, can open a TFSA.

You can open as many TFSAs as you want, but the amount of money you can contribute is limited, no matter how many accounts you have.

The annual TFSA limit for 2021 is $6,000, which matches the amount set in 2020 and 2019.

That means you can contribute $6,000 to your TFSA this year. Since you can carry forward any unused contribution room, you may be able to contribute even more.

What is my TFSA contribution room?

While you’re limited with how much you can contribute each year, the good news is that your TFSA contribution room grows every year (minus any withdrawals).

Your contribution room is made of:

- Your yearly TFSA dollar limit

- Plus any unused contribution room since 2009

- Plus any withdrawals made in the previous year

Any withdrawals from your TFSA will be added back to your contribution room at the beginning of the next year.

So if you withdrew money from your TFSA in 2020, you can reclaim that contribution room this year.

What happens if I over-contribute to my TFSA?

Review the current and past limits before you open and contribute to a TFSA. And if you withdraw any money this year and hope to add it back to your TFSA, remember that you must wait until next year.

For example: if you withdrew $4,000 from your TFSA account, and deposit it again in the same year, you’re considered to have contributed $8,000 total to your TFSA.

Any excess contributions are subject to a TFSA interest rate – you’ll be taxed at a 1% penalty per month as long as the excess amount remains in your account.

What is the lifetime contribution limit for the TFSA?

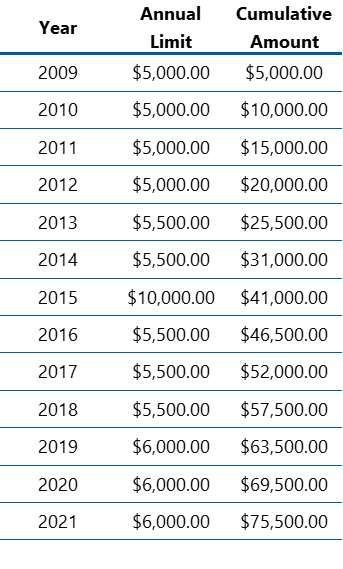

If you’ve never opened a TFSA before, you can deposit a hefty chunk of change to the account – $75,500 total (as long as you were 18 or older in 2009). Below is a chart listing the annual and cumulative limits since the program began:

Where can I find my TFSA contribution room?

You can check your TFSA contribution room through CRA MyAccount. Just note that this will usually show you the contribution room for the previous year, so don’t forget to include this year’s contribution. Otherwise you could be paying the TFSA interest rate.

How does a TFSA compare to a RRSP?

Unlike the Registered Retirement Savings Plan (RRSP), contributions to a TFSA are not tax deductible. But any amount you contribute is tax-free, even when it’s withdrawn. With an RRSP, you pay tax on withdrawals.

An RRSP is most beneficial for people who are in a higher tax bracket in their employment years and are looking to withdraw from the account in their retirement when they have a lower marginal tax rate.

If you’re a lower income earner, or saving for a vacation, a car or a down payment on a home, a TFSA will allow you to contribute up to $6,000 per year (or more depending on your contribution room) that you can withdraw anytime without penalty. And remember: investment gains are not subject to taxes.

Ideally you’ll be contributing to both accounts, since both beneficial to building savings.

For a comparison between the two, click here: Should I use an RRSP or TFSA as a business owner?

September 25, 2021: this blog was recently edited to correct the definition of TFSA annual contribution limits.

Contact FBC

When you join FBC, besides adding a tax team to your business, you’re also adding a team of financial advisors who can answer all your questions and help you plan for the future – FBC Financial and Estate Planning (FEPS).

Whether you’re thinking about the best way to save for retirement, want your kids to take over the family business someday, or are worried about the tax consequences of selling your business, we’re here to help you. There are a number of opportunities you can take to minimize your tax hit – but only if you plan in advance.

Want to learn more? We’re offering a free consult where we get to know your business and determine next steps on saving you money. Request a free consultation online.